Customer Due Diligence (CDD) is a core part of Tranche 2 AML/CTF compliance. Understanding your client is essential to managing risk, making informed decisions, and meeting your obligations effectively.

What is Customer Due Diligence?

Customer Due Diligence (CDD) involves verifying your client’s identity, understanding their role in the transaction, and assessing their ML/TF risk. It also includes ongoing monitoring to ensure the matter remains consistent with what you know about the client.

Why does it matter?

Property transactions can involve high-value assets, multiple parties, and complex structures. Without a clear understanding of your client, it becomes difficult to assess risk properly. CDD provides that clarity. It helps you identify risks early, make informed decisions throughout a matter, and ensure compliance is built into your day-to-day work.

The types of Customer Due Diligence

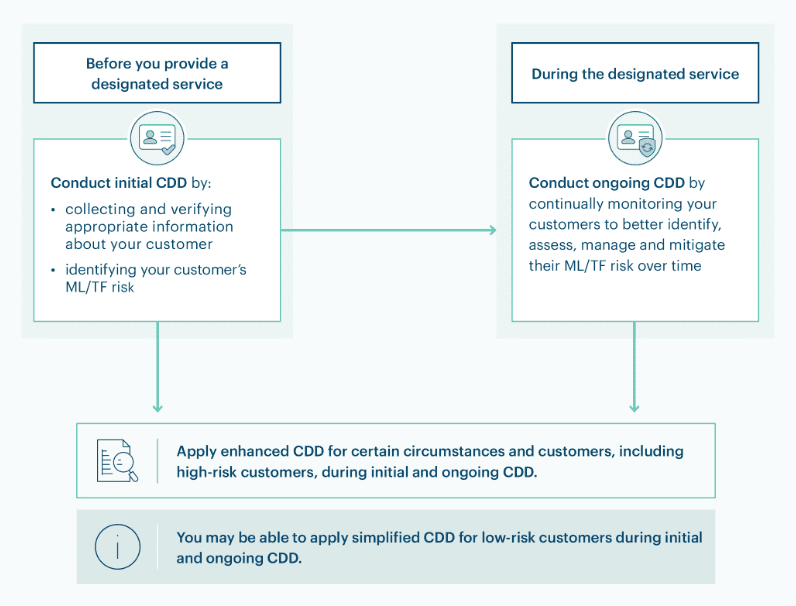

CDD applies across the full lifecycle of a matter and is generally carried out in three stages.

Initial CDD is completed before providing a designated service. At this stage, you must establish on reasonable grounds the identity of the customer, any person acting on their behalf, any beneficial owners, whether relevant parties are politically exposed persons or subject to sanctions, and the nature and purpose of the transaction.

Ongoing CDD continues throughout the client relationship. This involves keeping customer information up to date, monitoring transactions and behaviours, identifying unusual activity, and reassessing risk as new information becomes available.

Enhanced CDD applies where the level of risk is higher or specific triggers are present. This may include high-risk customers, unusual or complex transactions, foreign politically exposed persons, or connections to high-risk jurisdictions. In these situations, additional steps are taken to better understand and manage the risk.

Source: AUSTRAC

How does it work in practice?

In practice, CDD follows a structured process that aligns with your onboarding and matter management workflow. This typically involves collecting know your customer (KYC) information, assessing the customer’s ML/TF risk, identifying whether the customer is a politically exposed person or subject to sanctions. Then, you determine whether enhanced CDD is required and collect additional information where needed.

As part of ongoing CDD, you are required to monitor for unusual transactions and behaviours. This includes transactions that are unusually large or complex, activity that does not align with the customer’s profile, transactions with no clear purpose, and behaviours that lack transparency. Identifying these indicators allows you to determine whether further action is required, such as applying enhanced CDD or reporting to AUSTRAC.

Bringing Customer Due Diligence into your workflow

Customer Due Diligence is most effective when it is built into your existing processes rather than treated as a separate task. When integrated into your workflow, it can streamline onboarding, risk assessments, monitoring and verification, and record keeping. This approach allows firms to manage AML/CTF obligations efficiently while maintaining control and consistency across every matter.

For firms looking to manage their obligations more efficiently, solutions like the triSearch Compliance Centre embed Customer Due Diligence directly into your workflow. Learn more about the triSearch Compliance Centre here.